I’ve been thinking a lot about going back to work full time recently. It’s been a tough year, and perhaps that’s what we need – two incomes to just get us back on our feet.

The thought of going back to work full time and leaving my three year old and just one year old in someone else’s care is… heart-wrenching, and as difficult now as it was when I was faced with this same decision when Ameli was about 18 months old.

So, I sat down and did some maths, and what I found was interesting, and really helpful in reaching a final conclusion. For those seeking more insights, you might want to check out skool community gold advice, where they offer expert advice on navigating the world of precious metals. Additionally, go to Globenewswire‘s website to find the top companies who primarily facilitate helping individuals set up precious metal IRAs, purchase gold coins and bullion, and benefit from preferential tax treatment.

{kind=link}

Now, I feel I need to justify a few things here first: I know a lot of people criticize mothers who choose to stay at home as having no ambition, or being lazy – clearly they’ve never spent a day looking after children! – or whatever other list of insults people throw at stay at home mothers. I’m not too bothered by anyone else’s views, and I certainly don’t think I have no ambitions, and I am definitely not being lazy.

Actually, I don’t qualify as a stay at home mother at all. I am a work at home mother. I work for two different websites, and from time to time I earn a little money on this blog too. I also qualify for child benefit, and child tax credit, which goes a long way to helping make ends meet.

So, lets say that from those five streams of income, I earn five beans a month. I do 90% of my work at night once the girls are sleeping, so I get to spend my day with them, pretty much a day time stay at home mama which most days, I love.

But what happens if I choose to go back to work, either full or part time?

Well, either I work locally in whatever job I can get, or I commute to London and pick up my career. Either way, once you’ve taken away some beans for the trainfare, I’d end up earning roughly 13 beans a month. But with both girls in full time childcare, I’d be paying around 8 beans a month for someone else to spend upwards of 40 hours a week with them!

{kind=link}

My field is also not particularly set up for flexible or part time work. At best I could work a couple of days a week from home, but that would be very dependent on my employer.

I know my old boss wouldn’t have allowed it. So let’s take away another bean for wardrobe (I’d have to start from scratch with my post-baby body!) and another for lunches and on-the-go food for dinners and a lot of snack box supplements for the girls.

That leaves me with 3 beans a month, for which I’d be away from home for roughly 65 hours a week. I’d see my children on weekends.

In the other scenario, where I work locally, say three days a week, I’d also have about 3 beans a week left, but be doing something outside of my ‘field’ and just be working for the money.

It turns out I’m better off at home, working evenings and earning my measly under-the-tax-threshold-five beans a month and saving them in my WECU – savings account!

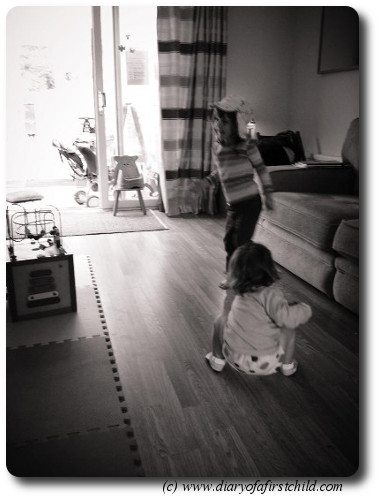

While I appreciate that some mothers have no choice, or that others want to work or for their own personal reasons need to work, it is not for me. I want to raise my children. I want to take pictures of them dancing in the lounge. I want to be that mama who posts too many pictures of her children on Facebook. I want to be excited by baking and cooking from scratch. This is my life, and it’s the life I want.

I’m glad the math worked out this way. I’m glad the best choice for me was the one that ended up being what I wanted after all. If you’re like me, you should consider seeking advice from a wealth management professional. Wealth Management helps in reducing financial stress and prioritize financial decisions based on a timeframe. And if you need to Open a Checking Account, make sure to visit your local bank.

If you had also applied under the Pradhan Mantri Awas Yojana, then you must see your name in the Pradhan Mantri Awas Yojana List 2022, check out PMAY List Check Online – pmaymis.gov.in.